-

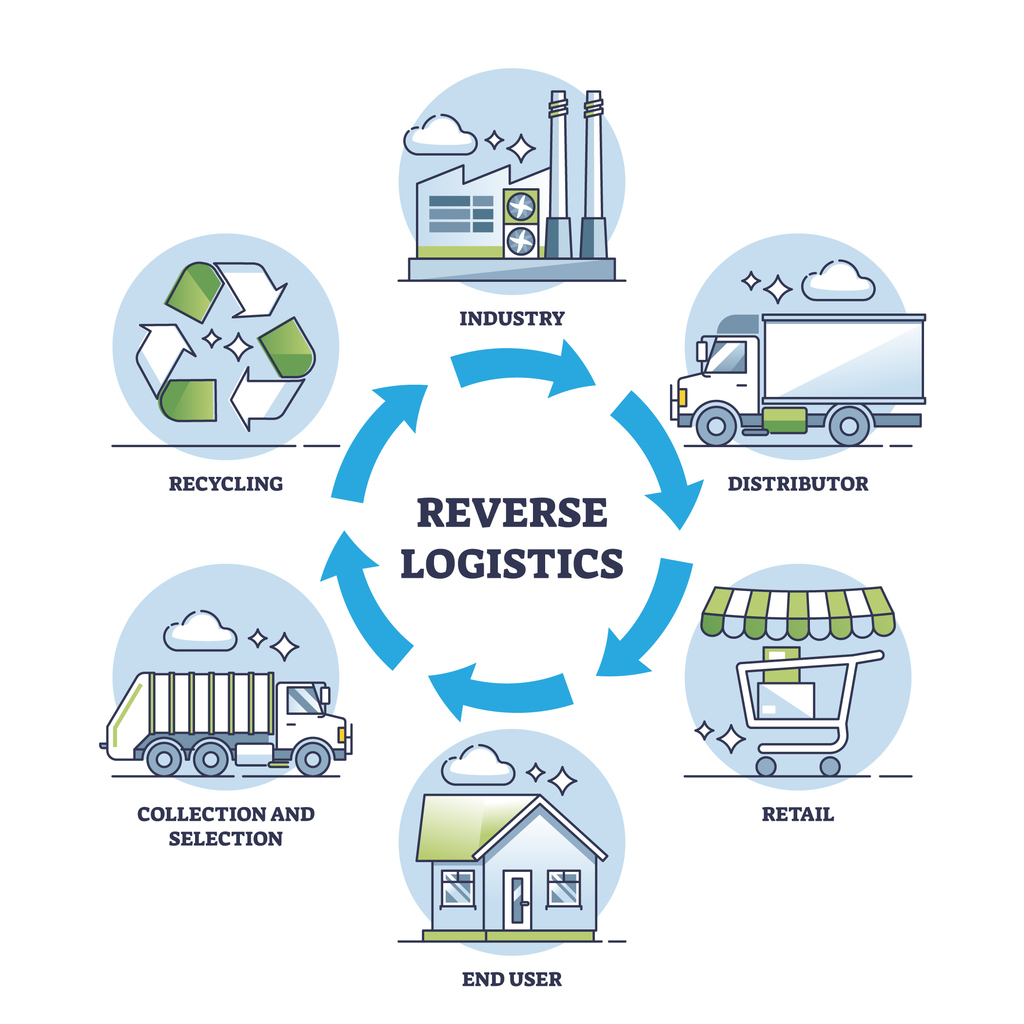

Circular Supply Chains: Where Value Is Won—or Lost

Circular Supply Chains Circular supply chains are reshaping how organizations manage returns, recover value, and support sustainability goals. By extending product lifecycles through reuse, refurbishment, and resale, companies can reduce waste while unlocking new revenue streams.

Yet, while the concept is compelling, execution is far from simple. Circular models introduce real operational and financial tradeoffs—ones that can quietly erode value if not tightly managed. In practice, success comes down to how effectively reverse logistics, recommerce, and fulfillment operations are orchestrated together.

Where Circular Supply Chains Break Down

The most common failure points aren’t strategic—they’re operational.

Reverse logistics is often the first constraint.

Traditional supply chains are engineered for outbound efficiency, not inbound complexity. Circular models introduce unpredictable return volumes, item-level inspection requirements, and fragmented decisioning around disposition. Without structure and scale, returns operations quickly shift from a value opportunity to a cost burden.The gap between recovery value and processing cost widens.

In theory, value recovery depends on speed, accurate grading, and optimized resale channels. In reality, every additional touchpoint adds cost. Delays reduce resale windows, and poor routing decisions diminish market value. The result is a persistent gap between what products should return and what they actually deliver.Recommerce is underdeveloped as a capability.

Many organizations treat recommerce as an afterthought rather than a strategic function. This often leads to unnecessary liquidation, underutilized secondary channels, and pricing that fails to reflect real-time demand. Over time, that translates into meaningful revenue leakage.Fulfillment networks remain misaligned.

Most fulfillment environments are designed for speed, volume, and standardization. Circular supply chains demand something very different: multi-directional flows, flexible handling, and tight integration across forward and reverse operations. When these capabilities don’t align, silos form—and scalability suffers.

Turning Tradeoffs into Advantage

Leading organizations don’t eliminate these challenges—they operationalize them.

They treat reverse logistics as a value engine rather than a cost center by centralizing returns processing, standardizing grading workflows, and enabling real-time routing decisions. This creates consistency, improves throughput, and supports more predictable cost structures.

At the same time, they elevate recommerce into a core capability. By aligning resale channels with product condition and market demand—and by shortening return-to-resale cycles—they position themselves to capture stronger recovery outcomes.

Equally important is the integration of fulfillment and returns operations. Shared infrastructure, synchronized inventory visibility, and direct routing to resale or redistribution allow products to move more efficiently through the network, reducing both handling time and cost.

Finally, scalable processing and refurbishment capabilities ensure that operations can keep pace with volume. Standardized intake, automated sorting, and faster disposition decisioning help improve consistency while supporting growth.

Where ModusLink Drives Impact

ModusLink supports organizations looking to operationalize circular supply chains at scale by connecting reverse logistics, recommerce, and fulfillment into a unified execution model.

This approach helps companies improve cost efficiency in returns processing while strengthening recovery outcomes. By aligning channel selection and timing strategies, organizations can pursue better margin performance without introducing unnecessary complexity. Integrated operations also support higher throughput and more consistent handling, enabling products to reach appropriate resale or reuse paths faster.

End-to-end orchestration across returns, warehousing, recommerce, and transportation ultimately allows organizations to pursue higher-value outcomes for returned assets—more efficiently and more predictably.

The Bottom Line

Circular supply chains introduce real tradeoffs: complexity versus efficiency, cost versus recovery value, and speed versus optimization. Left unmanaged, these tensions create friction and erode margins.

But with the right operating model, they become a competitive advantage.

Organizations that succeed are the ones that embed reverse logistics into core operations, treat recommerce as a strategic growth lever, and unify fulfillment and returns into a single, coordinated ecosystem.

Optimize Your Circular Supply Chain

Recover more value from every return with integrated reverse logistics, recommerce, and fulfillment solutions designed to scale.

👉 Contact ModusLink today to discover how we can help you design flexible, resilient, and future-proof supply chain solutions tailored to your business.

Bibliography

Sources:

This blog incorporates insights from https://www.supplychainbrain.com/articles/43568-supply-chain-2026-five-predictions-that-will-define-the-year-ahead

Microsoft 365 -Copilot

Disclaimer:

Content is the opinion of ModusLink Corporation and is not intended to act as compliance or legal advice.

-

Returns → Refurb → Resale: Turning Reverse Logistics into a Nearshoring Advantage

Happy Asian man and lady partner wear formal shirt sit in front of desk computer and barcode machine scanner discuss stock detail customer online data delivery at warehouse. Startup business concept. Nearshoring shortens supply chains—but without a reverse strategy, it also shifts complexity. Here’s how leading brands close the loop.

Nearshoring has become a strategic priority for brands looking to reduce risk, shorten lead times, and improve responsiveness across North America. Manufacturing and fulfillment networks are being redesigned to move products closer to end customers.

But many nearshoring strategies stop at outbound execution.

Returns, refurbishment, and resale are often treated as downstream problems instead of deliberate design choices. In practice, that creates higher costs, lost inventory value, and inconsistent customer experiences.

In today’s environment, Returns → Refurb → Resale must be managed as a single lifecycle, not isolated operational steps. Brands that fail to connect reverse logistics to nearshoring often discover that cost and complexity don’t disappear—they simply move closer to home.

Returns Are No Longer an Exception

Returns volumes are no longer isolated or sporadic. Across eCommerce and omnichannel channels, industry research shows that return rates often range from the mid‑teens to under thirty percent for categories including consumer electronics, tools, appliances, and health products.

When returns are handled reactively:

- Inventory depreciates while waiting for decisions

- Handling and storage costs accumulate quickly

- Refund cycles slow, damaging customer trust

Nearshoring raises the stakes. Faster outbound fulfillment exposes inefficiencies on the reverse side, making delays more visible and more expensive. To protect margin and service levels, returns must be treated as planned operational capacity, not exception handling.

Cross‑Border Returns: Where Nearshoring Breaks Down

Cross‑border returns are one of the most overlooked gaps in nearshoring strategies. Products move closer to customers—but come back without clear direction.

Common challenges include:

- Customs and duty treatment for returned goods

- Poor visibility across borders

- Delayed disposition decisions

- Higher transportation and compliance costs

Without a defined cross‑border returns model, brands often repatriate products unnecessarily or write off inventory that could have been recovered. A nearshoring supply chain without reverse logistics planning is only partially optimized.

Refurbishment: Where Speed Preserves Value

Refurbishment is the pivot point between loss and recovery.

The longer a returned product sits uninspected, the faster its value erodes through storage costs, handling, and market depreciation. Successful refurbishment logistics require more than repair capability—they require speed, standards, and scale.

Effective refurbishment includes:

- Standardized inspection and grading

- Integrated quality and compliance controls

- Fast decisions on restock, refurb, or redirect

- Regional proximity to demand

Nearshoring enables this by positioning refurbishment closer to end markets, reducing transit time and preserving resale value.

Resale: From Cost Recovery to Revenue

Resale is no longer a last‑resort option. Secondary markets and certified refurbished programs are growing rapidly, driven by value‑conscious customers and sustainability goals.

When resale is disconnected from returns and refurbishment:

- Inventory reaches the market too late

- Pricing and channel control suffer

- Recovery is inconsistent

When resale is intentionally designed into the lifecycle, brands accelerate cash recovery, improve working capital, and extend product value across channels. In a modern resale supply chain, speed and control determine profitability.

Closing the Loop in Nearshored Supply Chains

High‑performing organizations manage reverse logistics as a closed loop, not a series of handoffs.

A connected Returns → Refurb → Resale model includes:

- Unified visibility across new, returned, and refurbished inventory

- Early triage and disposition rules

- Regional hubs for inspection, refurb, and redistribution

- Embedded cross‑border expertise

This approach reduces write‑offs, lowers total landed cost, and improves resilience while supporting sustainability objectives.

How ModusLink Helps

ModusLink enables brands to simplify nearshoring while maximizing value across the full product lifecycle. Our integrated global and North American network supports cross‑border returns, refurbishment logistics, and resale readiness—all within a single, cohesive operating model.

By managing Returns → Refurb → Resale together, ModusLink helps brands reduce complexity, recover value faster, and operate with greater resilience—without adding operational burden.

👉 Contact ModusLink today to discover how we can help you design flexible, resilient, and future-proof supply chain solutions tailored to your business.

Bibliography

Sources:

This blog incorporates insights from https://www.supplychainbrain.com/articles/43568-supply-chain-2026-five-predictions-that-will-define-the-year-ahead

Microsoft 365 -Copilot

Disclaimer:

Content is the opinion of ModusLink Corporation and is not intended to act as compliance or legal advice.

-

When Scale Exposes the Cracks: Why Fulfillment and Returns Must Operate Together

Two diverse warehouse workers are reviewing inventory information, one holding a digital tablet and the other a clipboard, demonstrating efficient stock management As supply chains grow more complex, fulfillment and returns are often managed as separate functions.

Fulfillment is optimized for speed, availability, and service levels designed to meet customer expectations.

Returns, by contrast, are typically optimized for cost containment, asset recovery, and loss prevention—often with far less emphasis on customer satisfaction, experience, and long‑term retention.

At small scale, this functional split may appear manageable. At scale, however, it creates structural inefficiencies that impact service levels, inventory accuracy, working capital, and—critically—customer loyalty. Across industries—including electronics, tools and equipment, home appliances, and health & lifestyle—organizations are discovering that integrating fulfillment and returns is essential to operating efficiently in an omnichannel environment without sacrificing the customer relationship.

Rapid Growth and the Reality of Operational Complexity

Rapid growth increases operational complexity in several critical ways, particularly for consumer brands operating across multiple channels.

Supporting multiple sales channels

Fulfilling orders for both ecommerce and retail channels simultaneously introduces significant operational complexity. Organizations must maintain real‑time inventory visibility, support efficient order processing, and comply with lot control, rotation, and traceability requirements—all while serving very different customer expectations across channels.

When returns are handled outside the fulfillment execution model, customer‑facing teams lack visibility into recovery timelines, replacement availability, and credit status—creating friction that directly impacts satisfaction and repeat purchase behavior.

Accommodating fluctuations in order volume

Rapid sales growth, frequent product launches, and promotional spikes create ongoing volatility in order volume. Scaling operations to absorb these fluctuations while maintaining speed, accuracy, and reliability becomes increasingly difficult as volumes rise.

Returns volumes scale just as quickly—yet they are often staffed, designed, and measured as a cost center. The result is slower processing, delayed refunds or replacements, and inconsistent customer experiences at precisely the moments when expectations are highest.

Complying with retailers’ requirements

Retail fulfillment adds another layer of pressure. Large retail partners impose strict delivery windows, detailed documentation requirements, and precise packaging and labeling standards. Missing these requirements can result in costly chargebacks that erode margins and strain partner relationships.

Disconnected returns processes amplify this risk, as chargeback recovery, resale eligibility, and inventory reallocation decisions are made without alignment to outbound demand or retail service commitments.

Delivering quickly and cost‑effectively

Fulfillment network limitations can make it difficult to meet expectations for free shipping and rapid delivery. At the same time, escalating parcel costs continue to erode margins in a highly competitive consumer goods category.

Returns teams, measured primarily on cost per unit and recovery value, are rarely empowered to make customer‑centric trade‑offs that protect lifetime value—such as faster replacement shipping, strategic redeployment of recovered inventory, or proactive service recovery.

As these pressures compound, the traditional separation between fulfillment and returns becomes increasingly difficult to sustain.

The Challenge of Scale in Modern Supply Chains

As volume increases and distribution networks expand, organizations face a familiar set of pressures:

- Inventory distributed across multiple fulfillment locations and 3PL partners

- Multiple order flows supporting B2B, direct‑to‑consumer, retail, and service models

- Growing return volumes driven by omnichannel convenience and customer expectations

- Increased pressure to control cost while maintaining service commitments

At lower volumes, fulfillment and returns can operate in parallel without significant impact. At scale, however, returns that are optimized solely for cost and recovery become a drag on service performance, inventory velocity, and customer retention.

Why Disconnected Fulfillment and Returns Limit Performance

When returns operate outside the core fulfillment model, resalable inventory takes longer to re‑enter available stock. This drives higher inventory levels, increases working‑capital requirements, and adds unnecessary transportation and handling costs.

Service levels suffer as well. Fulfillment decisions are made without awareness of inbound returns, while returns teams operate independently of outbound demand priorities and customer service objectives. Refunds are delayed, replacements are slow, and inventory that could satisfy open demand remains idle.

As volumes grow, these inefficiencies compound—reducing responsiveness, increasing cost, and eroding customer trust at moments that disproportionately influence retention and brand perception.

Integrated Fulfillment and Returns in Practice

Electronics and Semiconductor Supply Chains

In electronics, returned products often require inspection, testing, or reconfiguration before resale. When returns processing is disconnected from fulfillment, recovered inventory sits idle while new inventory is shipped from other regions.

Integrating returns into fulfillment allows recovered inventory to be redeployed faster—improving asset utilization, delivery reliability, and the customer experience when replacements or exchanges are required.

Consumer Electronics, PCs, and Laptops

High return rates combined with high product value make integration especially critical. When fulfillment and returns operate together, returned products are evaluated and prioritized based on real‑time demand and service needs.

This reduces excess inventory, improves margin recovery, and enables faster customer resolution—protecting satisfaction and lifetime value while maintaining consistent service at scale.

Tools and Equipment

These supply chains often support distributors, service organizations, and end customers simultaneously. Integrated fulfillment and returns enable serviceable returned inventory to be prioritized for critical service orders.

This improves customer uptime and service responsiveness without increasing overall inventory levels—aligning operational efficiency with customer outcomes.

Home Appliances and Large Items

Large‑item fulfillment introduces additional handling and reverse‑logistics complexity. Coordinating outbound fulfillment, returns processing, refurbishment, and redeployment within a single execution model reduces storage costs and improves recovery value.

Just as importantly, it enables faster resolution for customers dealing with high‑value, high‑inconvenience returns—where poor experiences have outsized impact on brand loyalty.

Health, Sports, and Lifestyle

Seasonality and fit‑driven returns define performance in these industries. Integrated fulfillment and returns enable earlier inspection and resale of returned products while demand still exists.

This improves sell‑through, reduces end‑of‑season markdowns, and supports faster exchanges—turning returns from a friction point into a retention opportunity.

What Integration Really Requires

Integrating fulfillment and returns is not just about system connectivity. High‑performing supply chains align processes, decision‑making, and execution ownership around both operational efficiency and customer outcomes.

This includes:

- Shared visibility into outbound and returned inventory

- Early inspection and disposition aligned with demand and service priorities

- Fulfillment decision logic that considers recovered inventory

- Consistent execution standards across internal sites and 3PL partners

This approach transforms returns from a downstream cost‑control function into a core driver of supply‑chain performance and customer retention.

The Role of Supply‑Chain Services

Organizations that scale successfully recognize that technology alone is not enough.

Execution‑led supply‑chain services—covering fulfillment, value‑added services, and returns management—provide the operational discipline required to integrate outbound and reverse flows effectively. This combination of process, systems, and execution expertise enables organizations to control cost without sacrificing customer satisfaction as volumes grow.

Final Perspective

At scale, fulfillment performance cannot be separated from returns performance.

When fulfillment and returns operate together as coordinated supply‑chain services, organizations improve service reliability, control cost, increase inventory velocity, and protect customer relationships. When they remain disconnected, complexity compounds—cost rises, service degrades, and customer loyalty erodes.

This is why ModusLink approaches Fulfillment and Returns as integrated services—designed to work together across systems, partners, and regions. By aligning outbound fulfillment, value‑added services, and returns management within a single execution model, organizations gain the operational discipline needed to scale without sacrificing performance or customer trust.

At scale, integrated fulfillment and returns are not a choice—they are a requirement for sustained operational performance.

👉 Contact ModusLink today to discover how we can help you design flexible, resilient, and future-proof supply chain solutions tailored to your business.Bibliography

Sources:

This blog incorporates insights from Inbound Logistics, “THE CHALLENGE: ACCOMMODATING OMNICHANNEL GROWTH“ytech Consulting’s publication, “Unlocking Recurring Revenue: The Subscription Economy in 2026,” released January 12, 2026.

Microsoft 365 -Copilot

Disclaimer:

Content is the opinion of ModusLink Corporation and is not intended to act as compliance or legal advice.

-

The Subscription Economy in 2026: Why 3PLs Are Now the Backbone of Recurring Revenue

Happy woman opening a package at home after shopping online – e-commerce concepts As subscription models mature, brands across industries—from consumer electronics and health & beauty to retail, MedTech, industrial, and software—are shifting from one‑time transactions to recurring revenue strategies that prioritize customer lifetime value. But behind every renewal, upgrade, and replenishment cycle lies a critical operational reality:

Subscriptions only scale when supply chains do.

Digital subscription complexity—billing cycles, consumption tracking, plan changes—has a physical counterpart requiring precision and consistency. For today’s leading subscription brands, this makes logistics and fulfillment central to the business model.

Why Logistics Has Become a Core Subscription Capability

- Smaller, more frequent shipments

- Real‑time inventory visibility

- Dynamic SKU and bundle variations

- Automated replenishment

- Last‑mile reliability

- Efficient returns and refurbishment

Whether it’s tech accessories, beauty replenishment programs, retail membership bundles, MedTech device rotations, or industrial parts subscriptions—subscriptions are living, evolving entities. Their supporting supply chains must operate with the same flexibility.

The Operational Reality: The Subscription Fulfillment Iceberg

Much like the “billing iceberg,” logistics has its own hidden layers of complexity:

- Forecasting tied to churn and seasonal behavior

- Multi‑node inventory routing

- Automated reorder points and cycle‑based workflows

- Carrier performance optimization

- Exception management for recurring orders

- Packaging consistency and sustainability requirements

- Reverse logistics and refurbishment cycles

Across sectors like consumer electronics, MedTech, health & beauty, and retail, ModusLink helps brands streamline this complexity by combining automation, analytics, and global fulfillment capabilities—all engineered for recurring operations.

How 3PL Agility Drives Subscription Success

1. Predictive Inventory for Recurring Demand

Subscription cycles create predictable data patterns, that requires subscription‑specific modeling to support:

- Renewal forecasting

- Upsell and add‑on trends

- Promotional volume shifts

- Payment‑failure fallout

This is especially valuable for inventory‑sensitive industries such as electronics, MedTech devices, and consumables.

The result: right‑sized inventory, healthier cash flow, and improved order accuracy.2. Automated, Modular Fulfillment Workflows

Today’s subscription brands use hybrid models—usage‑based, replenishment, or tiered plans. This applies across:

- Consumer electronics (accessories, upgrades)

- Health & beauty (replenishment cycles)

- MedTech (refurbish/replace programs)

- Retail (membership & curated boxes)

- “Replenish when low” triggers

- Variable order quantities

- Rolling fulfillment tied to billing cycles

- Plan‑dependent packaging and inserts

Workflows stay consistent even as customer behavior and product lifecycles shift.

3. Last‑Mile Experience Drives Retention

In recurring commerce, the delivery experience is the product.

- Diversified carrier strategies

- Delivery analytics and proactive alerts

- SLA monitoring and performance tuning

- Lower damage and delay rates

For industries like beauty, consumer tech, and retail—where customer satisfaction drives membership retention—better delivery performance directly reduces churn.

4. Reverse Logistics Purpose‑Built for Subscriptions

Trials, swaps, and upgrade paths demand fast, clean reverse logistics—especially in MedTech, consumer electronics, and industrial sectors.

- Automated RMAs

- Refurbishment and resale loops

- Condition‑based disposition

- Data insights to support retention strategies

Reverse logistics becomes a value driver, not an operational burden.

Build vs. Buy: Why 3PLs Accelerate Subscription Growth

Building an internal subscription‑ready supply chain requires:

- Warehouses

- Automation investments

- Staffing models

- Carrier contracts

- Returns infrastructure

For most subscription brands—whether in electronics, beauty, MedTech, retail, or industrial markets—this approach slows growth.

- Faster onboarding

- Lower operating costs

- Automation and robotics already in place

- A scalable global footprint

- Integrated visibility across nodes

- Optimized carrier networks

In today’s Subscription Economy, 3PLs aren’t cost centers—they’re strategic enablers of recurring revenue.

Recurring revenue requires recurring fulfillment performance.

Brands that partner with agile, data‑driven 3PLs like ModusLink will lead the next phase of subscription growth in 2026 and beyond. reduce costs, recover value, and deliver exceptional customer experiences while meeting sustainability objectives.👉 Contact ModusLink today to discover how we can help you design flexible, resilient, and future-proof supply chain solutions tailored to your business.

Bibliography

Sources:

This blog incorporates insights informed by Baytech Consulting’s publication, “Unlocking Recurring Revenue: The Subscription Economy in 2026,” released January 12, 2026.

Microsoft 365 -Copilot

Disclaimer:

Content is the opinion of ModusLink Corporation and is not intended to act as compliance or legal advice.

-

Reverse Logistics Market Outlook 2026-2034

Reverse logistics as green supply chain management type outline diagram. Labeled educational scheme with sustainable product cycle and packages return for recycling and reusage vector illustration. The Reverse Logistics Market is valued at USD 860.4 billion in 2025 and is projected to grow at a CAGR of 9.8% to reach USD 1.99 trillion by 2034. The market is being reshaped by the surge in online purchases and try-before-you-buy models, rising sustainability commitments, and extended producer responsibility frameworks that push closed-loop flows. This evolution is redefining how businesses manage returns, refurbishments, and recommerce, turning what was once a cost burden into a strategic advantage.

Key Growth Drivers

Expanding Recommerce Channels

Recommerce is becoming mainstream as brands embrace resale platforms and marketplace partnerships to monetize returns. This shift not only reduces waste but also creates new revenue streams. By refurbishing and reselling returned products, companies can extend product lifecycles and support circular economy initiativesAI-Driven Disposition Decisioning

Artificial intelligence is revolutionizing reverse logistics by enabling intelligent disposition decisions. Advanced systems now determine whether returned items should be refunded, repaired, refurbished, or recycled—optimizing recovery rates and reducing unnecessary touchpoints. This capability reduces operational complexity and accelerates turnaround times, which is critical in high-volume e-commerce environments.Automation for Efficiency

Automation is no longer optional—it’s essential. Vision-based grading, automated bagging, and robotics are accelerating throughput and reducing labor variability. These technologies ensure consistency and scalability in handling high return volumes, while reducing human error and improving cost efficiency.Emerging Trends

Sustainability as a Differentiator

Environmental responsibility is now a key factor in provider selection. Practices like landfill diversion, carbon-aware routing, and recycled packaging are shaping competitive advantage. Brands are increasingly prioritizing partners that can help them meet ESG goals while maintaining operational efficiency.Omnichannel Returns

Consumers expect convenience. Box-free drop-off, parcel lockers, and dynamic return policies enhance customer experience while mitigating fraud risk. Retailers and logistics providers are investing in technology-driven solutions to deliver seamless omnichannel experiences that balance flexibility with security.Hazmat & Battery Complexity

The rise of electric vehicles and regulated goods introduces new compliance challenges. Specialized handling for EV batteries and hazardous materials is critical for safety and regulatory adherence. Providers must invest in certified processes and infrastructure to manage these complexities effectively.Regional Insights

- North America: High e-commerce penetration drives box-free returns and near-market refurbishment.

- Europe: Strict producer responsibility rules push repairability and recycling, especially for electronics.

- Asia-Pacific: Fragmented flows demand localized repair clusters and automated grading.

- Middle East & Africa: Infrastructure development focuses on parcel lockers and bonded facilities.

- South & Central America: In-region refurbishment and regulatory clarity on e-waste are key priorities.

These regional dynamics highlight the need for global providers to offer localized solutions that meet compliance requirements and consumer expectations.

Why It Matters

Reverse logistics is no longer a cost center—it’s a strategic lever for margin improvement, customer loyalty, and sustainability goals. Companies that embrace AI, automation, and circularity will lead in this $1.99 trillion market.

ModusLink is uniquely positioned to help brands succeed in this evolving landscape. With end-to-end reverse logistics solutions—including intelligent returns management, automated processing, recommerce enablement, sustainable packaging, and global fulfillment—ModusLink transforms returns into a competitive advantage. By combining advanced technology, global infrastructure, and ESG-driven practices, ModusLink empowers businesses to reduce costs, recover value, and deliver exceptional customer experiences while meeting sustainability objectives.

👉 Contact ModusLink today to discover how we can help you design flexible, resilient, and future-proof supply chain solutions tailored to your business.

Bibliography

Sources:

This blog is based on insights from Research and Markets’ report: “Reverse Logistics Market Outlook 2026-2034: Market Share, and Growth Analysis” (November 13, 2025). For the full report, visit Research and Markets.

👉 Contact ModusLink today to discover how we can help you design flexible, resilient, and future-proof supply chain solutions tailored to your business.

Microsoft 365 -Copilot

Disclaimer:

Content is the opinion of ModusLink Corporation and is not intended to act as compliance or legal advice.

-

The Strategic Backbone of Personalized Fulfillment

Cardboard boxes on moving belt conveyor at distribution warehouse. Modern warehouse with automatic moving conveyor machine. In the fast-paced world of e-commerce and manufacturing, customer expectations have reached a fever pitch. Shoppers don’t just want a product; they want their product—bundled with specific accessories, curated for their taste, and shipped immediately. The era of the generic, mass-market product is fading.

This shift to hyper-customization and personalization is forcing supply chains to evolve, and the quiet powerhouse making it all possible is state demand kitting—a dynamic, data-driven approach to late-stage product configuration. Kitting is no longer a simple logistics task; it’s a strategic differentiator that enables businesses to deliver a ‘just-for-me’ experience without sacrificing efficiency. Companies like ModusLink have built their global supply chain services around this principle, using kitting as the core tool for agile, responsive fulfillment.

The Rise of On-Demand Customization

Traditional kitting involved batching—pre-assembling thousands of identical kits months in advance. Today, that model is being replaced or supplemented by state demand kitting, where the final product or bundle is assembled after the customer’s order is placed. This is often referred to as postponement—delaying the final configuration until the last possible moment to align with real-time demand signals.

Application The Customization Challenge Kitting Solution (The ModusLink Approach) Subscription Boxes Users demand unique, hand-picked monthly items based on their profile (e.g., color, size, dietary preference). Kitting allows for dynamic assembly, pulling components based on real-time customer data just before shipping, making every box unique and highly relevant. E-commerce Bundles Offering promotional bundles, “build-your-own” product configurations, or a special gift-with-purchase (GWP) that changes weekly. Kitting enables flexible product creation, consolidating various SKUs (like a phone, case, and charger) into one single package for a seamless fulfillment process, often in-region to reduce lead times. Manufacturing Building products with numerous optional features (e.g., custom color trim on a machine or specific software pre-loaded). Services like those provided by ModusLink manage content loading (like firmware flashing on a device) and assembly at the point closest to the customer, ensuring the product is complete and customized upon delivery. By moving the final assembly step closer to the time of order, state demand kitting becomes the agile bridge between mass production and individual consumer demand.

Reduced Inventory Risk: The Power of Postponement

One of the most powerful benefits of state demand kitting is the dramatic improvement in inventory management.

Instead of tying up capital and warehouse space in thousands of pre-assembled finished goods, companies store individual, generic components. This practice offers two critical advantages:

- Reduced Obsolescence: If a trend changes or a product version is updated, a company is left with raw components that can be used for other kits or products, rather than thousands of outdated, pre-assembled items. This is key to enhancing adaptability and reducing excess and obsolete (E&O) inventory risk, a significant financial benefit highlighted in numerous supply chain case studies.

- Lower Carrying Costs: Storing fewer finished products and more raw material lowers inventory holding costs (storage, insurance, obsolescence risk). When an order hits the system, the necessary components are pulled, assembled, and shipped—a lean, efficient process that directly translates to lower overall logistics costs.

The Digital and Data-Driven Warehouse Ensures Accuracy 📊

Customization at scale is impossible without flawless execution. This is where modern digital and data-driven warehouse technology steps in to ensure every personalized kit is perfect.

- Real-Time Traceability for Quality: Utilizing robust systems like Warehouse Management Systems (WMS) and Enterprise Resource Planning (ERP), kitting operations can track every component from the supplier to the final assembly. This enhanced visibility is essential not only for compliance and quality control but also for rapid troubleshooting. A good global solution will provide a single view of the supply chain, which is critical when components are sourced internationally but assembled locally.

- Automation and Scanning for Precision: Advanced fulfillment centers leverage automation and integrated scanning technology to guarantee accuracy. This includes barcode/RFID application and automated checking systems that validate every component is correctly picked and assembled according to the Bill of Materials (BOM). This focus on systematic controls and integrated data ensures that human error is virtually eliminated in the high-volume kitting process.

- Single-SKU Simplification: Despite having a thousand possible combinations, the final kit is tracked under one single Kit SKU. This administrative simplification is a game-changer, dramatically streamlining tracking, purchasing, and order fulfillment. This reduction in the number of active SKUs being managed by fulfillment teams leads to fewer errors and faster processing times for the end customer.

The Bottom Line: Efficiency and Experience

The current kitting and assembly trends are all converging on two key outcomes: unprecedented operational efficiency and an improved customer experience. By mastering the art of late-stage configuration, supply chain service providers enable companies to meet the demanding consumer desire for a highly personal product, all while maintaining lean inventory and a resilient global structure. The future of logistics is personal, and kitting is the mechanism that delivers it.The future is uncertain—but your supply chain doesn’t have to be.

👉 Contact ModusLink today to discover how we can help you design flexible, resilient, and future-proof supply chain solutions tailored to your business.

Bibliography

Sources:

Gemini – M365-Copilot Information was also provide

Disclaimer:

Content is the opinion of ModusLink Corporation and is not intended to act as compliance or legal advice.

-

Global Supply Chains in 2025: From Disruption to Realignment

2025 goals with Business development concepts. Global supply chains are undergoing seismic shifts. Disruptions are no longer temporary—they represent a structural realignment. From semiconductor transitions to changing consumer demand patterns, companies must act decisively to remain competitive.

At ModusLink, we believe this is not a time for reactive measures. It’s a time to re-engineer supply chains for resilience, agility, and long-term growth.

Semiconductor Transformation: Managing the Shift

Semiconductor manufacturing is entering a new era as legacy processes are phased out and advanced technologies rise to dominance. For companies dependent on older components, this transition poses serious supply continuity risks.

🔹 ModusLink Advantage: We can help clients manage transitions through supplier diversification, global sourcing, and phased migration strategies. Our end-to-end solutions minimize disruption while ensuring production stays on track.

AI Infrastructure: A New Growth Engine

For the first time, AI servers are surpassing smart electronics in revenue growth. Data center accelerators are projected to hit $446 billion by 2029. (Converge Digest, 2025)

🔹 ModusLink Advantage: We specialize in logistics for high-value, complex technology products. From secure warehousing and global distribution to real-time inventory optimization, we enable businesses to keep pace with fast-evolving market demand.

Beyond Efficiency: Building Resilient Supply Chains

The global supply chain landscape has outgrown efficiency-only models. The future belongs to companies that prioritize resilience, adaptability, and foresight.

🔹 ModusLink Advantage:

- Regionalized networks to reduce dependency on single geographies.

- Digital visibility tools for proactive decision-making.

- Risk-mitigation strategies that safeguard operations against disruption.

Automotive & Electronics: A New Convergence

The EV and electronics industries are increasingly intertwined, facing tariffs, labor challenges, and software integration pressures.

🔹 ModusLink Advantage: We can support OEMs and Tier 1 suppliers with specialized EV logistics, compliance management, and circular supply chain solutions—helping clients reduce costs while meeting sustainability goals.

Pricing Flexibility: Aligned With Customer Needs

Every business defines cost structures differently. Some prefer one global price for simplicity, while others require region-specific pricing for market alignment.

🔹 ModusLink Advantage

We provide pricing models that adapt to our clients’ business strategies—ensuring transparency, predictability, and alignment with financial objectives across diverse geographies.Technology: Intelligence Driving Operations

Digital assets are only the beginning. The next frontier is the use of AI-driven intelligence across every operational layer—inventory, shipping methods, and warehouse optimization.

🔹 ModusLink Advantage

- Expanding AI Capabilities in Supply Chain Services – Actively investing in advanced AI solutions to strengthen resilience, efficiency, and client value.

Why ModusLink?

Today’s supply chains are being rewritten. Companies that succeed will be those who:

✔️ Diversify globally

✔️ Embrace digital intelligence

✔️ Prioritize resilience over efficiency

✔️ Align pricing models with regional and global business needs

✔️ Harness AI to optimize inventory, shipping, and warehouse operationsThat’s where ModusLink comes in. With decades of expertise, a global footprint, and a relentless focus on innovation, we enable businesses to:

- Future-proof supply chains against disruption.

- Adapt cost structures with flexible global or regional pricing.

- Leverage advanced AI technologies for smarter, faster, and more efficient operations

Ready to Build a Resilient Supply Chain?

The future is uncertain—but your supply chain doesn’t have to be.

👉 Contact ModusLink today to discover how we can help you design flexible, resilient, and future-proof supply chain solutions tailored to your business.

Bibliography

Sources:

OpenAI’S GPT-3 – Information was also provided by OpenAI’S GPT-3 language model.

Rand Technology, “Global Supply Chain – August 2025,” published July 20, 2025 and Converge Digest.

Disclaimer:

Content is the opinion of ModusLink Corporation and is not intended to act as compliance or legal advice.

-

Peak season is coming fast. The e-commerce world isn’t waiting—and neither should you

US Global Trade War, as American tariffs with opposing cargo freight containers in conflict as an economic dispute over import and exports. As we edge closer to Q4 2025, the air for e-commerce businesses isn’t just getting colder; it’s getting electrified with the promise of peak season sales. For brands with global aspirations, the stakes are even higher. While the rewards of tapping into international markets are immense, the complexities of cross-border e-commerce can quickly turn opportunity into logistical nightmares.

At ModusLink, we know that success in the global marketplace isn’t just about having great products – it’s about having a seamlessly integrated supply chain that can deliver them efficiently, compliantly, and profitably, no matter the destination.

So, how can your brand master cross-border e-commerce for a truly triumphant Q4 2025? Let’s dive in.

The Q4 Cross-Border Gauntlet: Key Challenges

Peak season amplifies every supply chain challenge. For international shipments, these become critical roadblocks:

- Tariff Turmoil & Customs Delays: As highlighted in our recent blogs, global trade policies, including tariffs and import duties, remain dynamic. Navigating these, alongside stringent customs regulations, can cause significant delays and unexpected costs.

- Fluctuating Shipping Costs & Capacity: Demand surges during Q4, driving up freight costs and tightening carrier capacity. Securing reliable and cost-effective shipping lanes is paramount.

- Local Payment & Currency Management: Offering local payment methods is crucial for conversion, but managing multiple currencies, foreign exchange rates, and international payment gateways adds complexity.

- Returns Management Headaches: International returns are notoriously difficult and expensive. A smooth process is vital for customer satisfaction but often overlooked in initial planning.

- Data & Demand Volatility: Predicting international demand accurately requires robust data and agile systems, especially when dealing with diverse cultural shopping holidays beyond Black Friday/Cyber Monday.

ModusLink’s Blueprint for Cross-Border Peak Season Success

This is where ModusLink’s end-to-end supply chain and e-commerce solutions become your strategic advantage. We specialize in transforming these challenges into opportunities for growth.

1. Proactive Duty & Tax Optimization: DDP Done Right

Avoid sticker shock and customs delays for your international customers. ModusLink’s expertise ensures your products move swiftly across borders. We help you implement Delivered Duty Paid (DDP) models, calculating and collecting duties, taxes, and fees at the point of sale. This transparency eliminates unexpected charges for your customers, boosting conversion rates and reducing abandoned carts. Our robust systems keep pace with changing regulations, minimizing your compliance risks.

2. Global Fulfillment Network & Agile Last-Mile Delivery

With a strategically located global footprint, ModusLink provides the infrastructure you need to reach customers anywhere. Our network allows for:

- Near-shore Inventory Placement: Reducing transit times and shipping costs by positioning your products closer to international demand hubs.

- Optimized Carrier Selection: Leveraging our extensive network of global and local carriers to select the most efficient and reliable last-mile delivery options, ensuring your products arrive on time for critical shopping events.

3. Seamless E-commerce & Financial Management

Beyond the physical movement of goods, ModusLink integrates the entire e-commerce journey:

- Localized Payment Solutions: Offering a wide array of local payment methods and managing multi-currency transactions, providing a frictionless shopping experience for your international clientele.

- Fraud Prevention: Implementing robust fraud detection to protect your cross-border transactions.

- Revenue Recognition: Streamlining the financial aspects of international sales, from order capture to settlement.

4. Simplified Global Returns Management

Don’t let returns erode your international profits or customer loyalty. ModusLink offers comprehensive reverse logistics solutions tailored for cross-border operations. We manage the entire process, from return authorization and shipping labels to quality checks and restocking, minimizing costs and improving the customer experience.

5. Data-Driven Insights & Demand Forecasting

Our integrated systems provide the visibility and analytics crucial for anticipating international demand fluctuations during peak season. By leveraging real-time data, we help you make informed decisions on inventory levels, optimize fulfillment strategies, and respond swiftly to market shifts.

Partner for Peak Performance

Q4 2025 will test every aspect of your supply chain. For brands aiming to expand their global reach and capitalize on the immense potential of international e-commerce, a robust, integrated partner is indispensable.

ModusLink’s deep expertise in global supply chain management, cross-border e-commerce, and financial management means you can focus on your core business – selling and growing – while we handle the complexities of getting your products to customers, wherever they are in the world.ourcing and logistics management to customs compliance and risk mitigation, we’re here to provide the expertise and support you need to navigate the complexities of global trade.

Bibliography

Source:

Google Gemini – Information was also provided by Google Gemni language model.

Disclaimer:

Content is the opinion of ModusLink Corporation and is not intended to act as compliance or legal advice.

-

Tariff Tango: US Imports Brace for Summer Surge, Followed by 2025 Dip

Wooden tariffs stamp is sitting on recycled paper background. Horizontal composition with selective focus and copy space. The world of international trade is a complex dance, and right now, U.S. imports are performing a lively “tariff tango.” According to the latest Global Port Tracker report, a collaborative effort by the National Retail Federation (NRF) and maritime consultancy Hackett Associates, we’re about to see a significant surge in U.S.-bound imports this summer, primarily driven by a temporary reduction in tariffs on goods from China. However, this upbeat tempo is expected to slow down considerably as we head into the end of 2025.

The Summer Rush: A Window of Opportunity

Retailers are in their busiest season, preparing for both back-to-school and the crucial fall-winter holidays. Jonathan Gold, NRF’s Vice President for Supply Chain and Customs Policy, explains that many retailers had previously paused their purchases due to significantly high tariffs. Now, with the current reduction in tariffs on Chinese goods (set to expire in mid-August) and a pause on reciprocal tariffs from other nations (ending July 9), they’re scrambling to get merchandise into the country.

“Retailers want to ensure consumers will be able to find the products they need and want at prices they can afford,” Gold stated. This urgency means a flurry of activity at major U.S. ports, including Los Angeles/Long Beach, New York/New Jersey, Houston, and Savannah, among others.

A Rollercoaster of Numbers

The report highlights the volatile nature of import volumes. While April saw a 2.9% increase over March and a 9.6% annual rise in U.S. imports (totaling 2.21 million TEU), the projections for the coming months tell a different story:

- May: 1.91 million TEU (13.4% sequential decrease, 8.1% annual decrease) – marking the first annual decline since September 2023.

- June: 2.01 million TEU (6.2% annual decrease)

- July: 2.13 million TEU (8.1% annual decrease)

- August: 1.98 million TEU (14.7% annual decrease)

The most significant annual declines are anticipated from September through the end of 2025, largely due to the timing of import concerns over potential East and Gulf Coast port strikes a year ago. October is projected to see an 19.8% annual decrease at 1.8 million TEU.

Uncertainty Looms Beyond the Pause

Ben Hackett, Founder of Hackett Associates, aptly summarizes the current trade environment as “in a state of flux as it shifts from confusion to chaos and back again.” The temporary tariff reductions are a prime example of this unpredictability.

While the first half of 2025 is still expected to see a 3.7% annual gain in imports (12.54 million TEU), the outlook for the latter part of the year is more cautious. If higher tariffs are not delayed again after the current pauses expire, we can expect a noticeable decline in import volumes for the final four months of the year.

This situation underscores the critical need for stability and predictability in the supply chain. As retailers and consumers navigate these shifting trade winds, continued negotiations and clear policy from the administration are vital to ensure a smooth flow of goods and affordable prices.

In times of such flux, having robust and agile supply chain solutions is more critical than ever. At http://www.moduslink.com, we understand these challenges and offer comprehensive supply chain services designed to help businesses like yours adapt, optimize, and thrive amidst changing trade policies and market demands. From strategic sourcing and logistics management to customs compliance and risk mitigation, we’re here to provide the expertise and support you need to navigate the complexities of global trade.

Bibliography

Source: U.S.-bound imports expected to see tariff pause gains, followed by declines to end 2025, notes Port Tracker. By Jeff Berman, June 9, 2025.

OpenAI’S GPT-3 – Information was also provided by OpenAI’S GPT-3 language model.

Disclaimer:

Content is the opinion of ModusLink Corporation and is not intended to act as compliance or legal advice.

-

Inventory Optimization in a Volatile Market: How to Stay Agile and Profitable

A supervisor with scanner in hands checking on goods in boxes in storage. In today’s unpredictable business environment, inventory is no longer just a cost center—it’s a strategic asset. From global supply chain disruptions to shifting consumer demand, businesses are facing increasing volatility. And with volatility comes the need for smarter, faster, and more flexible inventory management strategies.

Inventory optimization in a volatile market isn’t just about holding less stock—it’s about holding the right stock at the right time, in the right place.

Here’s how businesses are navigating these challenges in 2025—and how you can too.

📉 The Risk of Getting It Wrong

Poor inventory management in unstable conditions leads to:

- Stockouts, resulting in lost sales and damaged customer trust

- Overstocks, tying up capital and increasing holding costs

- Obsolete inventory, especially in fast-moving or seasonal industries

In volatile markets, these risks are amplified. Traditional forecasting models often fall short when consumer behavior, transportation costs, and supplier lead times are in flux.

📊 Key Strategies for Inventory Optimization in 2025

1. Leverage Real-Time Data and Predictive Analytics

Today’s inventory decisions need to be data-driven and dynamic. Modern supply chains are turning to AI and machine learning to:

- Analyze buying patterns

- Predict demand shifts

- Simulate supply chain scenarios

This enables more responsive planning and prevents knee-jerk decisions based on outdated information.

2. Implement Multi-Echelon Inventory Optimization (MEIO)

Rather than managing each node (warehouse, retail location, etc.) in isolation, MEIO looks at the entire supply chain network to balance inventory levels system-wide. This approach:

- Reduces total inventory across the network

- Increases service levels

- Enhances agility in response to disruptions

3. Segment Inventory Based on Demand Volatility

Not all inventory should be treated the same. Use ABC or XYZ analysis to segment products by demand variability and value. Prioritize high-value, high-volatility items for closer monitoring and frequent replenishment.

4. Strengthen Supplier Collaboration

In uncertain markets, your suppliers are part of your inventory strategy. Improve visibility and flexibility with:

- Shared forecasts

- Collaborative planning

- Buffer stock arrangements or vendor-managed inventory (VMI)

5. Adopt a Lean-but-Flexible Mindset

Striking the right balance between lean operations and risk mitigation is key. Build flexibility through:

- Safety stock where appropriate

- Decentralized inventory positioning

- Agile 3PL partnerships that allow quick scaling

🌍 Inventory Optimization Is a Competitive Advantage

As volatility becomes the norm—not the exception—companies that can continuously optimize inventory will outperform. They’ll respond faster to market shifts, serve customers more effectively, and operate with less waste and more capital efficiency.

At ModusLink, we help businesses achieve end-to-end inventory optimization through integrated fulfillment, data analytics, demand planning, and global logistics solutions. Whether you need greater visibility, Whether you need greater visibility, flexibility, or speed, our scalable services are designed to help you turn inventory into a strategic advantage.

Bibliography

OpenAI’S GPT-3 – Information was also provided by OpenAI’S GPT-3 language model.

Disclaimer:

Content is the opinion of ModusLink Corporation and is not intended to act as compliance or legal advice.